Market Context

May 2026

Live market data · Updated May 31

S&P 500 at 7,580.06. VIX at 15.32 (normal). WTI crude at $87.36.

System operating with standard parameters — signals evaluated systematically

regardless of prevailing narrative. No prediction, only systematic response.

Market Snapshot — May 31

S&P 500

7,580.06 +0.22% today

VIX (volatility)

15.32 regime normal

WTI Crude Oil

$87.36 -1.73% today

NASDAQ Composite

26,973 +0.20% today

Our Algorithm

The system runs on defined risk per trade —

every entry has a stop, every exit is automated, every regime change adjusts position size.

When VIX is elevated, size drops or trades pause. When structure aligns, the algorithm

engages without hesitation.

Designed to survive shocks — not by predicting them, but by

refusing to trade when conditions don't meet criteria.

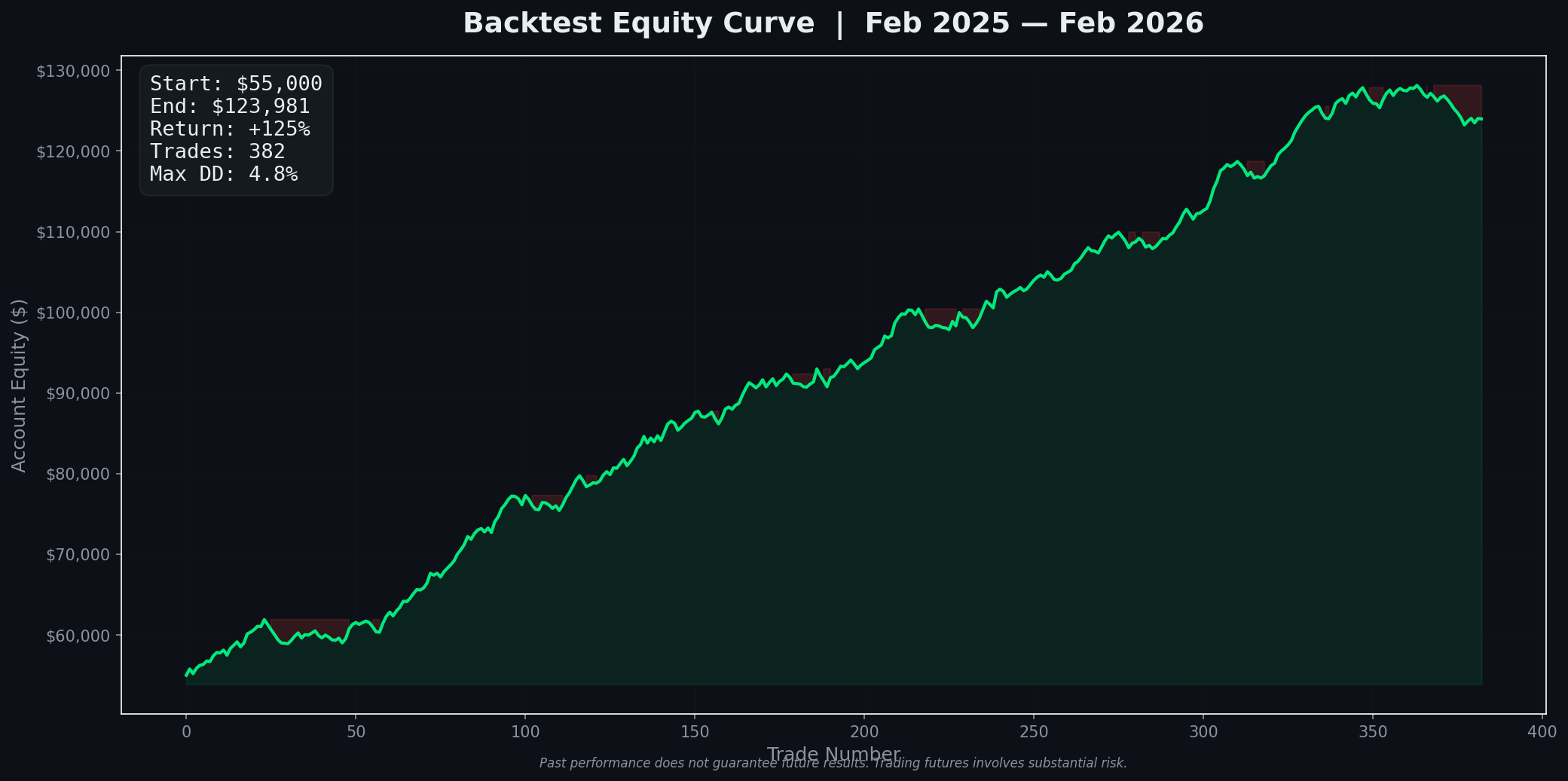

Every trade published. Every win, every loss.

Current regime: VIX 15.32 (normal). System operating with standard parameters.

Current Month

May 2026 —

VIX at 15.3 (normal).

14 trades this month, 2W / 9L.

System operating with standard parameters.

External data from public financial reporting. No claim of outperformance is made or implied.

Past performance does not guarantee future results.